ETFs, Liquidity and Cashing Out

Table of Contents

I've written about ETFs, and how they're pretty much the best option for anyone that just doesn't have the time or interest in diving into the depths of stock picking.

I also made a post comparing the different types of Halal ETFs, and their performance — by far my most popular post on this site. However, I missed one key consideration in that post: a measure of the liquidity of a given ETF.

In this post, I'll describe what liquidity is, how to measure it (in the case of ETFs), a ranking of the halal ETFs by liquidity and how to place ETF orders to the maximum effect.

Let's dive in.

What is Liquidity?

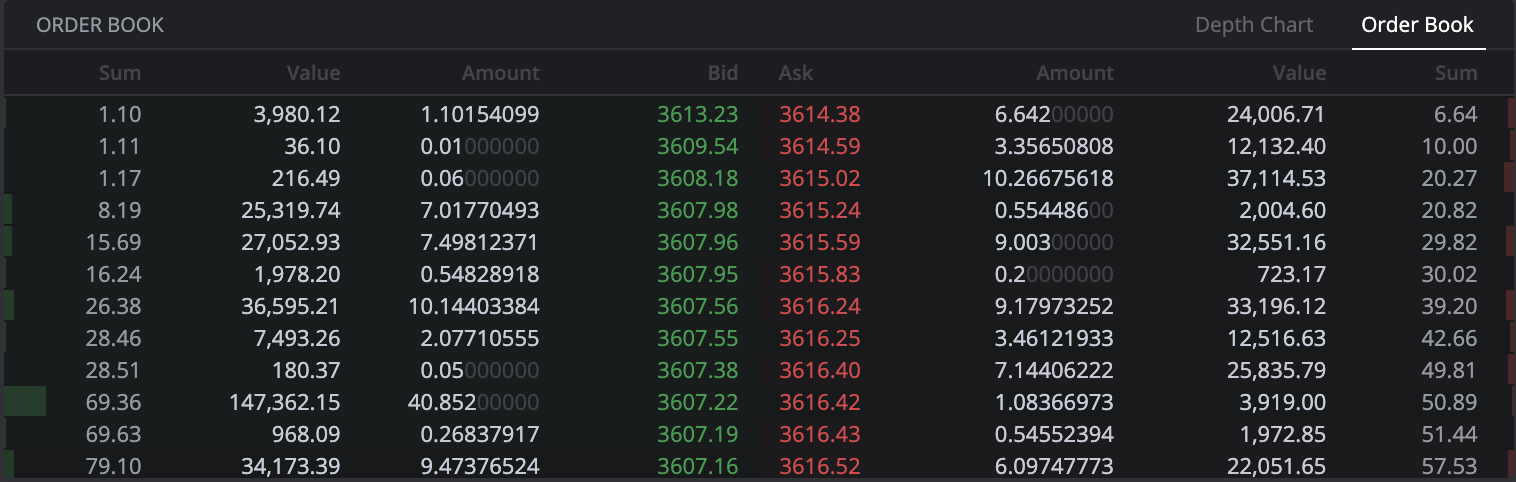

When you buy or sell a stock, the price that you see is really the average of 2 numbers: the Bid and the Ask. The bid is the highest price that any buyer is currently willing to pay; the ask is the lowest price any seller is willing to accept.

A "trade" takes place when a seller drops down to the bid price, or when a buyer pays a bit more and accepts the ask price.

Of course, the underlying assumption is that there's always a buyer and a seller, at any given time. This isn't always the case.

Which is why we have "market makers". Market makers buy from sellers and sell to buyers, usually pocketing a small profit in the process. They hold a variety of stocks for short periods of time, and chances are high that the bid & ask prices you see will always come from market makers.

Liquidity then is just a measure of how easy it is to get into and out of a stock.

If the stock you're trading has plenty of buyers and sellers, it's quick and easy. If not, then you'll be holding on to those bags for a while — just how long depends on how low you're willing to go to get rid of it.

All this talk about liquidity begs the question: how do you measure how liquid a given stock or ETF is?

Measuring the Liquidity of a Stock

The de facto measure of liquidity in a stock is the Bid/Ask spread. The Bid/Ask spread, as the name hints at, is the difference between the Bid and the Ask in USD. A tight spread (low $ value) is a sign of strong liquidity; a wide spread (high $ value) is bad.

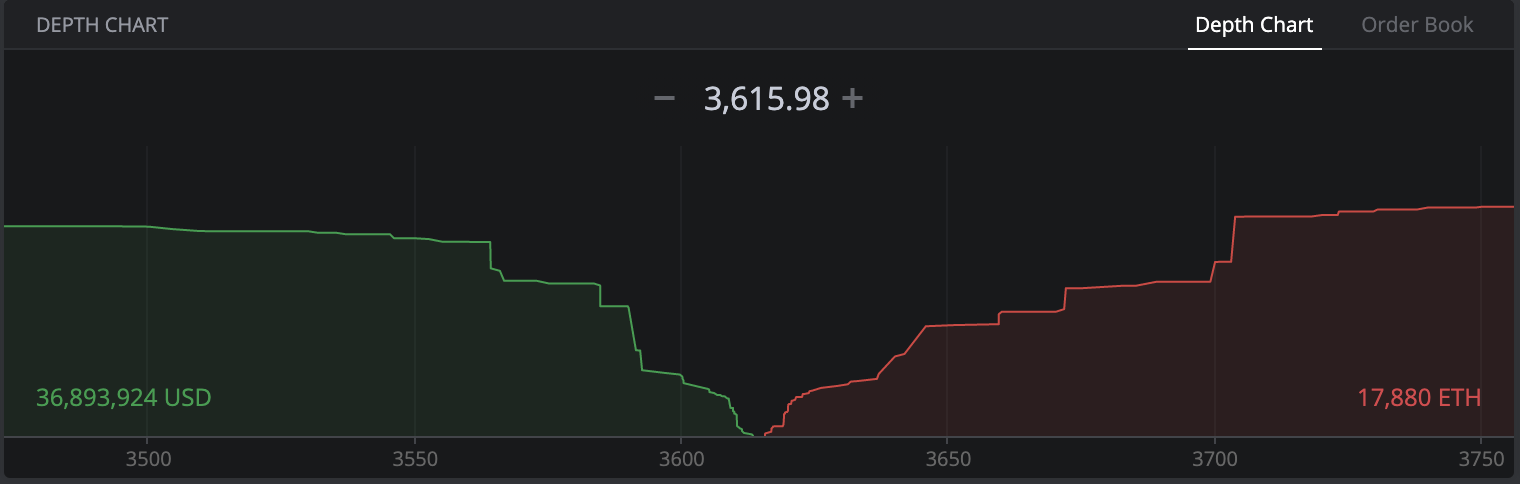

The spread itself is just the difference between the best bid and the best ask, but it's important to remember that there are other bids/asks:

If you plot these, you'll see what is essentially a mountain (the technical term is "depth chart"):

Wide bid/ask spreads are a real concern, especially for those of us that have experience trading OTC stocks or microcaps. You could place an order well within the bid/ask spread and still not see it execute for hours, or even days.2

ETF liquidity considerations

There are a few special considerations when it comes to ETFs.

See, ETFs aren't like normal stocks. Stocks are just, well, stocks. They represent a share in a company. The price of a stock is purely market-based (it's just the middle of the bid/ask spread, as we mentioned above).

But ETFs aren't just tickers. They are also baskets of stocks, and they have an intrinsic worth: the value of the stocks in the proverbial basket (known as the "Net Asset Value" / NAV). The NAV per share (or "Intrinsic Value") is what actually matters in the long run. Generally speaking, an ETF will trade around the intrinsic value, but sometimes it drifts away1.

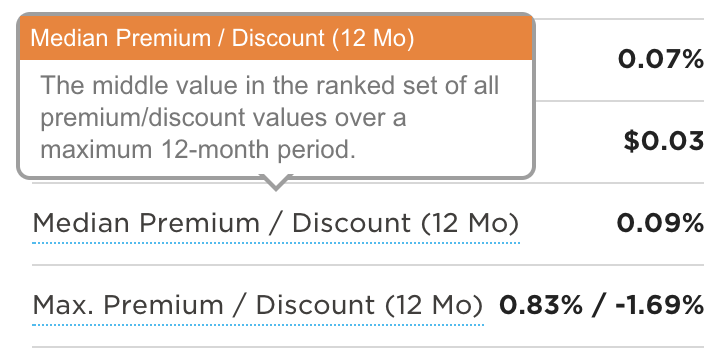

You want to buy into an ETF when the ticker price is trading close to NAV (or even at a discount to the NAV)3. This is why it's important to also consider the premium/discount that the ETF has historically traded at, relative to the stocks it holds.

This data can easily be retrieved. Here's a sample from ETF.com for $HLAL:

You want to trade ETFs where the NAV per share lies within the Bid/Ask spread (and, as ever, the tighter the bid/ask spread, the better!).

Comparing Liquidity of Halal ETFs

Now that we know what to look for, let's size up the main Halal ETFs against this criteria.

To recap, we're looking for:

- Bid/Ask spread

- Premium/Discount to NAV

Here's what the numbers look like (as of 17th May, 2021):

| Ticker | Bid/Ask Spread (%) | Median Premium (1y) | Max. Premium (1y) |

|---|---|---|---|

| HLAL | 0.07% | 0.09% | 0.83% / -1.69% |

| SPUS | 0.23% | 0.21% | 1.55% / -0.50% |

I searched for data on ETFs domiciled outside the US (ISDU, ISDW, ISDE) but was unable to find any. (If you know where to get, please let me know.

Between the two listed above, it's clear that HLAL is the superior pick.

How to buy ETFs efficiently

This bit is important, so listen closely.

Never place a market order when purchasing ETFs, especially if you're buying large amounts (e.g. $10,000+/order).

Always, always use Limit orders and set the limit to the Net Asset Value of the ETF you're purchasing. That way, you know you're getting your basket's worth. You may even end up buying it for less than what the basket is worth (yaay!), but no higher.

Additional Reading

If you're interested in learning more, check out some of the sources I referenced below:

- https://www.etf.com/etf-education-center/etf-basics/understanding-etf-liquidity?nopaging=1

- https://www.investopedia.com/articles/exchangetradedfunds/08/etf-liquidity.asp

- https://www.proshares.com/media/documents/etf_structure.pdf

- https://etfmarketpro.com/does-volume-matter-evaluating-etf-liquidity/

- https://www.thestreet.com/investing/etfs/how-market-makers-profit-on-etfs-10568719

- With thinly traded stocks, you may be tempted to just buy at the asking price (if you're trying to get into a stock). But then you're essentially paying a premium for quick execution. It's almost always better to buy at the Bid + a small amount, resulting in your order becoming the best bid (and thereby resulting in a narrower bid/ask spread).↩

- In theory, whenever there's a difference between the ETF price and the price of the underlying assets, an "Authorized Participant" swoops in to create/destroy ETF shares by buying/selling the underlying shares.↩

- However, you can't actually sell at NAV. At least, not unless you've got some serious volume on your hands (25,000+ shares, or roughly $700k worth). In that case, you can trade in the "primary market" by calling up the ETF issuer's capital market desk.4. They'll put you through to an “authorized participant” (AP) who's authorized to change the supply of ETF shares available — either by offloading a large basket of shares (“redeeming” shares) or buying a large basket of shares (“creating” shares). For retail investors that don't trade these kind of volumes, you'd rely on the secondary market (driven by market makers) instead.↩