Valuing Companies Using The DCF Method

Discount Cash Flow (DCF) is arguably the most popular method for valuing companies today. In this post, I explain exactly how it works and work through a recent example — applying the DCF method to arrive at a valuation for Stich Fix ($SFIX).

Learning how to value companies is the most important skill you'll need in your quest for undervalued opportunities.

The Discount Cash Flow method is used to estimate the money an investor would receive from an investment, adjusted for the time value of money.

The 'time value of money' describes the idea that a dollar today is worth more than a dollar tomorrow. To reach a target price for a company today, we essentially 'discount' future money into today's money … the further out it is, the greater the discount. That's what the 'discount' in Discounted Cash Flow means.

As you can guess from the name, we'll be discounting 'Cash Flow' — more specifically, future Free Cash Flow (FCF).

What is Free Cash Flow

Free cash flow is the cash that's available to a firm's investors, before getting distributed to debt holders, equity holders, or reinvested back.

Think of it as the cash that's free for the company to spend at the end of a period, ready to distribute to the different owners (either as payments to bond and equity holders) or for reinvesting back into the company.

Calculating Free Cash Flow

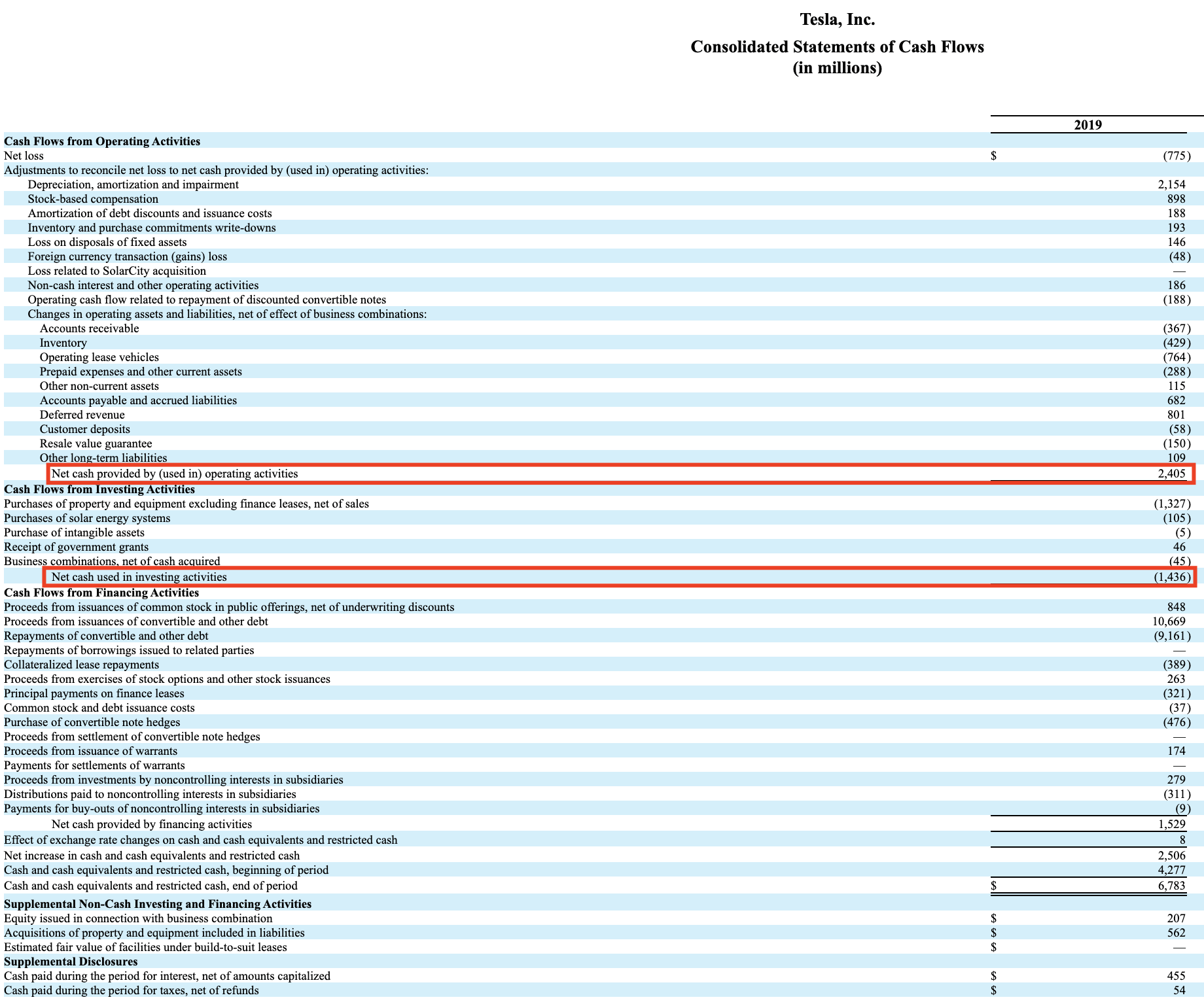

To make this more concrete, let's take a look at a snapshot of the 2019 Cash Flow statement for $TSLA 1:

It's a monstrosity of a table, but focus on the few items that matter:

Free Cash Flow = Net Cash From Operating Activities - Long Term Investments (PP&E)

Net Cash From Operating Activities is net loss (from the Income Statement), but after adding back all of the "accrued items" that didn't actually impact cash. These are things like depreciation, stock based compensation and some other stuff that's not paid for with cash. By excluding these items, we get just the things that affected the cash position of the company.

Long term investments (or Plants, Property & Equipment — PP&E, and sometimes referred to as Capital Expenditures — CapEx) is pretty much what you'd expect: any money spent on property, equipment and other capital expenditures.

The result is:

Free Cash Flow = $2,405m - $1,436m = $969m

Phew, that's our FCF!

Check out the next post to to see how we project Free Cash Flow into the future.